Kentucky VA Home Loans offered by a Kentucky Veteran. I have successfully originated over 100 VA Kentucky Mortgages for fellow Kentucky Veterans and active duty personnel.$0 Down Home loans in KY. Free Credit Report and free pre-approvals. I can be reached by text or call at 502-905-3708, or kentuckyloan@gmail.com Not affiliated with VA Government Agency. NMLS #57916 Company NMLS #1364 Former Army Tanker 19k

Kentucky VA loans make home ownership affordable for active servicemen and women, veterans and reservists even if the borrower has only been in active service for 90 days. We offer Jumbo VA loans up to 2 million. VA loans often enable borrowers to buy with no money down* and feature competitive rates and fees.

FUNDING FEE WAIVED FOR PURPLE HEART RECIPIENTS

Since VA Loan Funding Fees are 2.3% to 3.5% of the loan, this could save thousands! Veterans with disabilities and surviving spouses may also qualify to have their Funding Fee waived. Our customers deserve to be rewarded for their service.

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender.

Effective on all Kentucky VA Mortgage loans closed on or after January 1, 2020

The VA Home Mortgage program has amended funding fee percentages for all Kentucky Veterans (including Regular Military, Reserves, and National Guard) for loans closed on or after January 1, 2020 and before January 1, 2022.

As indicated above, the funding fee will no longer be determined by Regular Military, Reserves or National Guard status. Therefore, based on the Kentucky Veteran’s individual scenario, the funding fee may increase or decrease on or after January 1, 2020.

The Kentucky VA funding fee you pay in 2020 will depend on your down payment amount and whether you’ve ever had a VA-backed loan before. If you haven’t, it’s a “first use” loan, and if you have, it’s a “subsequent use” loan. You can pay the fee upfront or roll the cost into the loan.

The fee for first-use, zero-down loans will be 2.3% of the loan amount in 2020, up from 2.15% for regular military in 2019. The fee for subsequent use loans will be 3.6% of the loan amount, up from the current 3.3%. These fees will stay in place for two years, return to current levels from 2022 to October 2029 and drop further after that.

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant's eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

NTB standards apply to all cash-out refinancing loans.

The NTB consists of the NTB Test, Loan Comparison Disclosure, and the Home Equity Disclosure

NTB Test for Cash-Outs

All cash-out refinancing loans must pass the NTB test. The requirement is met if the refinancing loan satisfies one of the following:

The new loan eliminates monthly mortgage insurance; or

The loan term of the new loan is less than the loan term of the loan being refinanced; or

The interest rate of the new loan is less than the interest rate of the loan being refinanced; or

The monthly (principal and interest) payment of the new loan is less than the monthly payment of the loan being refinanced; or

The monthly residual income is higher as a result of the new loan; or

The new loan is used to payoff the interim construction loan; or

The new loan LTV is equal to or less than 90 percent of the reasonable value of the home; or

Refinance of an adjustable-rate mortgage to a fixed rate mortgage

Loan Comparison Disclosure

The lender must disclose to the borrower a comparison of the new loan to the existing loan being refinanced.

VA requires lenders to generate two loan comparison disclosures

One within three (3) business days of the initial loan application

One at closing

The borrower must certify receipt of both disclosures

The Initial 3-Day Disclosure requires lenders to provide a reasonably accurate estimate within three (3) business days of the application

The Final Loan Closing Disclosure “shall be accurate with respect to the new loan info, while the initial loan info may be a ‘generally accurate representation’ of the existing loan.”

Contents of the Initial 3-Day and Closing Disclosures include: refinancing loan amount v. payoff amount of refinanced loan; interest rate of each loan; mortgage loan type of each loan; term of each loan;total payments on each loan; and LTV of new loan v. loan payoff to current value of loan being refinanced

Home Equity Disclosure

Discloses the amount of equity being withdrawn, with explanation how removal of equity may affect the sale or refinance of the home in the future.

For initial equity disclosure, the lender may use estimated loan payoff or unpaid principal balance and estimated current property value to determine equity being removed.

For final disclosure at closing, lender must use final payoff amount and reasonable value shown on the Notice of Value.

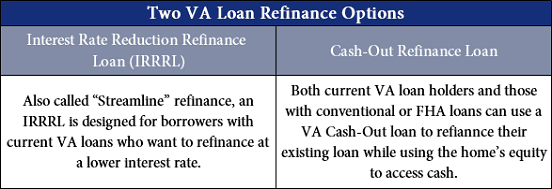

Net Tangible Benefit for IRRRL’s

INTEREST RATES

If the loan is fixed rate to fixed rate then the new loan rate must be at least 50 basis points better than the loan being refinanced.

If it is a fixed rate to ARM then the new rate must be at least 200 basis points better than the loan being refinanced.

DISCOUNT POINTS

The lower interest rate cannot be produced solely from discount points unless: Points are paid at closing;

- VA IRRRL’s with discount points require an exterior only appraisal to establish the LTV