10 facts about the Kentucky VA Home Loan program

1. No down payment, no mortgage insurance

These are perhaps the biggest advantages to a VA loan. You don’t need a down payment. None whatsoever. Most mortgage programs, such as FHA and conventional loans, require at least 3.5 percent to five percent down.That’s up to $12,500 on a $250,000 home purchase.

With a VA loan, you can buy immediately, rather than years of saving for a down payment. With a VA loan, you also avoid steep mortgage insurance fees. At 5 percent down, private mortgage insurance (PMI) costs $150 per month on a $250,000 home, according to PMI provider MGIC.

With a VA loan, this buyer could afford a home worth $30,000 more with the same monthly payment, simply be eliminating PMI. Using a VA loan saves you money upfront, and tremendously increases your buying power.

2. Use your benefit again and again

Your VA home loan benefit is not one-and-done. You can use it as many times as you want. Here’s how.

Assume you purchased a home with a VA loan. But now, you’ve outgrown the home and need something bigger. When you sell the home and pay off the VA loan completely, you can re-use your benefit to buy another home. Your entitlement is restored in full.

But that’s not the only way to re-use your benefit.

Eligible Veterans and Service persons can receive a one-time restoration when they pay off the VA loan, but keep the home. This scenario comes into play if you purchased the home long ago, and have paid off the loan. It also applies if you have refinanced the VA mortgage with a non-VA loan.

In these cases, you can keep the home, and enjoy the benefits of VA home buying one more time.

3. Your benefit never expires

Once you have earned eligibility for the VA home loan, it never goes away. Those who served 20, 30, even 50 years ago often wonder whether they can still buy a home today if they never used their benefit. If eligibility can be established, the answer is yes.

Eligibility is based on the length of time served, and the period in which you served. For instance, a U.S. Army Veteran with at least 90 days in service during the Vietnam era is likely eligible.

To check eligibility, first obtain your DD Form 214. With that document, a VA-approved lender can request your VA Certificate of Eligibility for you, or you can request it directly from VA’s eBenefits website. You may be eligible to buy a home using a VA home loan, even if you served long ago.

4. Surviving spouses may be eligible

More than 3,000 surviving spouses purchased a home with their fallen partner’s VA benefit in 2015. Un-remarried husbands and wives of Service-persons who were killed in action can buy a home with zero down payment and no mortgage insurance. Plus, the VA funding fee is waived.

There’s no way to repay the spouse of a fallen hero, but this benefit surely helps them move forward after tragedy.

5. VA Loan Rates Are Lower

According to loan software company Ellie Mae, VA loan rates are typically about 0.25% lower than those of conventional loans. The VA backs the mortgages, making them a lower risk for lenders. Those savings are passed on to Veterans.

Additionally, VA loans come with some of the lowest foreclosure rates of any loan type, further reducing risk for lenders. No surprise here, but Veterans and Service persons take home ownership seriously. These factors add up to lower rates and affordable payments for those who choose a VA loan.

6. VA loans are available from local lenders

The VA home loan is unlike most other VA benefits. This benefit is available from private companies, not the government itself. The Department of Veterans Affairs does not take applications, approve the loans, or issue funds. Private banks, credit unions, and mortgage companies do that.

The VA provides insurance to lenders. It’s officially called the VA guaranty. The VA assures the lender that it will be repaid if the Veteran can no longer make payments. In turn, lenders issue loans at superior terms. In short, a VA loan gives you the best of both worlds. You enjoy your benefit, but have the convenience and speed of working with your chosen lender.

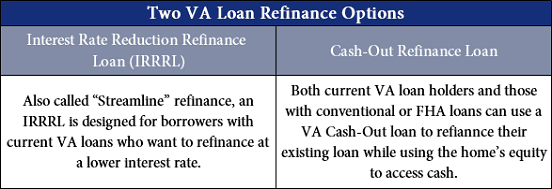

7. Buy, refinance or tap into home equity

The VA home loan benefit is not just for buying homes. Sure, it provides unmatched home buying advantages, but you can also use it to refinance your existing mortgage, whether it’s a VA loan or not.

Homeowners with a VA loan can use the Interest Rate Reduction Refinancing Loan, or IRRRL, to easily drop their rate and payment without an appraisal, or even paystubs, W2s or bank statements. The VA streamline refinance, as it is commonly known, gives VA loan holders a faster, cheaper way to access lower refinance rates when rates fall.

Even homeowners without a VA loan can use a VA refinance. The VA cash-out loan is available to eligible Veterans who don’t have a VA loan currently. As its name suggests, a VA cash-out refinance can be used to turn your home’s equity into cash. You simply take out a bigger loan than what you currently owe. The difference is issued to you at closing.

The VA cash-out loan amount can be up to 100 percent of your home’s value in many cases. Use the proceeds for any purpose – home improvements, college tuition, or even a new car.Many homeowners today are dropping their rate and taking cash out simultaneously, accomplishing two goals at once.

But you don’t have to take out cash to use this VA loan option. You can also use it to pay off a non-VA loan. Eligible homeowners who pay mortgage insurance or are dealing with other undesirable loan characteristics should look into refinancing with a VA loan. It can eliminate PMI, get you into a stable fixed-rate loan, pay off a second mortgage, or simply reduce your rate to make homeownership more affordable.

8. Lenient guidelines for lower credit scores, bankruptcy, foreclosure

Unlike many loan programs, a lower credit score, bankruptcy or foreclosure does not disqualify you from a VA home loan.

Shop around at various lenders, because each will have its own stance on past credit issues. However, VA guidelines do not state a minimum credit score to qualify. This gives lenders leniency to approve loans with lower scores. In addition, VA considers your credit re-established when you have established two years of clean credit following a foreclosure or bankruptcy.

Many homeowners across the U.S., military and civilian, experience bankruptcies and foreclosures due to a loss of income, medical emergency or unforeseen event. Fortunately, these financial setbacks don’t permanently bar VA-eligible home buyers from ever owning again.

The exception, though, is a foreclosure involving a VA home loan. In this case, you may need to pay back the amount owed on the foreclosed VA loan to regain eligibility. But for most home buyers with past credit issues, a VA home loan could be their ticket to home ownership.

9. Funding fee waivers

VA typically charges a funding fee to defray the cost of the program and make home buying sustainable for future Veterans. The fee is between 0.50 percent and 3.3 percent of the loan amount, depending on service history and the loan type.

However, not everyone pays the VA funding fee. Disabled Veterans who are receiving compensation for a service-connected disability are exempt. Likewise, Veterans who are eligible for disability compensation, but are receiving retirement or active duty pay instead, are also exempt from the fee.

10. Buy a condo with a VA loan

You can buy many types of properties with a VA loan, including a single-family (free-standing) home, a home of up to four units, and even manufactured homes. But condominiums are commonly overlooked by VA home buyers.

Condominiums are ideal starter homes. Their price point is often lower than that of single-family homes. And, condos are often the only affordable option in many cities.

The VA maintains a list of approved condominium communities. Veterans can search by city, state, or even condominium name on VA’s condo search tool. It’s not a short list.

As a Veteran or Service-member, consider the array of home types when shopping for a home.